Ron McMahan

Ron McMahan

1 min read

242 Cities Now Have $1M Starter Homes, What That Means for Real Estate Investors

The entry-level housing market just hit a new milestone, and not a good one for first-time buyers.

1 min read

The entry-level housing market just hit a new milestone, and not a good one for first-time buyers.

1 min read

Tsunami Warning Update: Inundation and Landfall Has Arrived The CRE Tsunami has now come ashore, causing valuations to decline significantly, demand...

1 min read

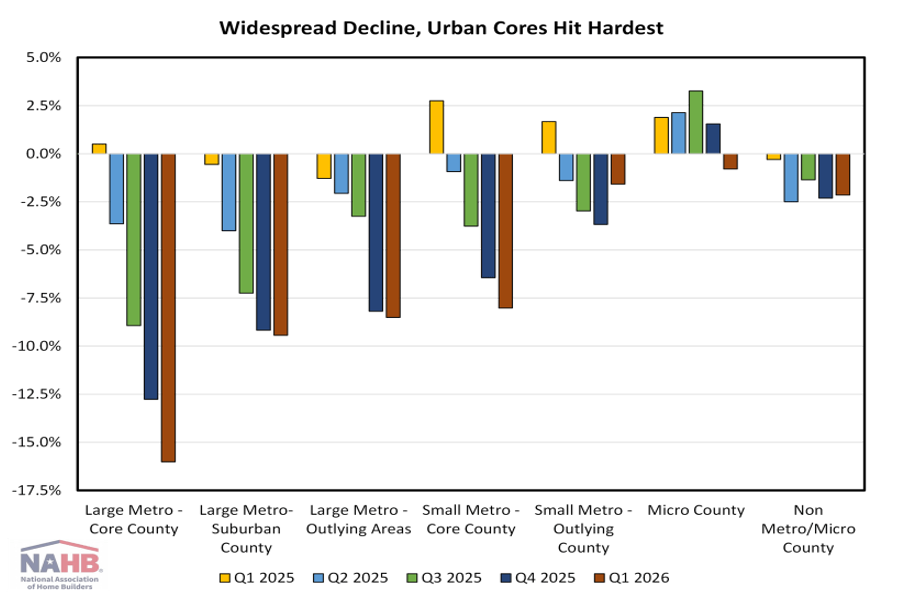

Single-family construction declined across all geographies in the first quarter of 2026, according to the latest Home Building Geography Index...